Bank Disasters

Silicon Valley Bank made a bunch of disastrous disclosures today.

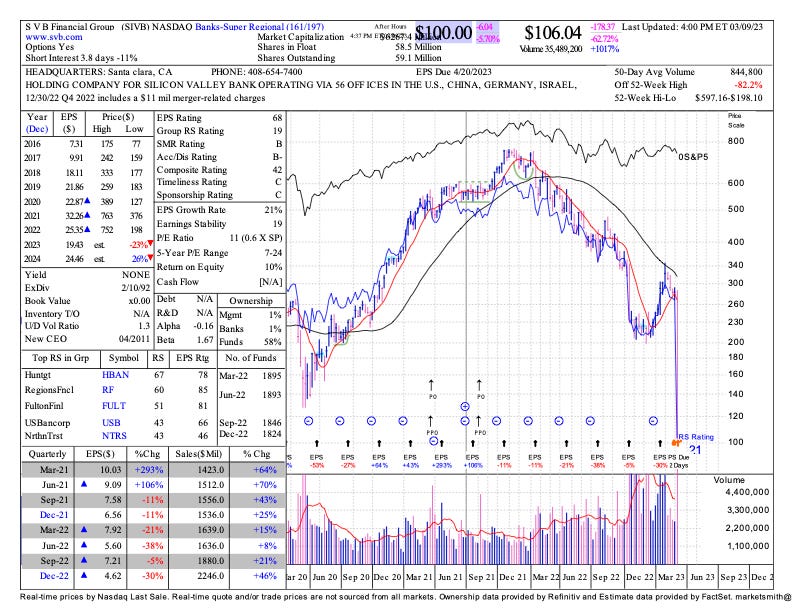

"Stay Calm" - Silicon Valley Bank CEO Reassures VC Clients Amid Sudden Liquidity Crisis

As kids, we used to call these “Smooth Moves”. We find a huge cluster of them in this announcement. This is not just about high technology and Silicon Valley. It is about the entire global banking system.

Bank Bloodbathery Sparks Widespread 'Risk Off'

And then there were Silvergate, Credit Suisse, and even J.P. Morgan along for the ride.

Many of us have been warning of this for a long time.

The global financial system relies on credit, not money. The only real money is gold and silver. All of the rest is loaned into existence. With an interest rate, to boot.

Don’t believe me? Take out a dollar bill from your purse or wallet. It says “Federal Reserve Note”. No longer convertible into silver. It is just a promise that somebody would accept it as payment.

Don’t believe me? J.P. Morgan himself, testifying in 1912:

“Gold Is Money. Everything Else Is credit.”

John Titus refers to it as “pseudo money”. It turns out that when you write a check to pay bills, the lender is not legally obligated to accept it to extinguish the debt. The second step requires their acquiesence. Only then can it be reflected on your balance due.

His video is below, and is a must view:

CBDC and the Fed's Plan to Weaponize Money

As you can see, he also covers Central Bank Digital Currencies. Fascinating information. Very dangerous plans afoot.

So who cares? Everyone should care. Almost no commerce could occur without credit. Every business and every individual with few exceptions would find it impossible to function except at a barter level. If the financial system is imploding, that means the supply of bank credit is shrinking. Rapidly. Perhaps in the early stages of collapsing.

Why is that important to a depositor at a bank? In the last financial crisis, we saw “bail-outs”. Bail-outs are impossible now. Governments are technically bankrupt. The central banks are insolvent. The Federal Reserve alone is carrying massive losses on their balance sheet against a capital base of just $50 billion. They claim their balance sheet is around $9 trillion. The off balance sheet items are unimaginably larger than that.

So if the system implodes, what do we get this time? Bail-ins. If you have money on deposit with a bank, you are an unsecured creditor. If the bank goes belly up, you are probably last in line to get your deposit back, if at all. Forget thinking this is “conspiracy theory”. It is settled law, and has been for centuries. The infrastructure for implementing bail-ins is already in place. Ignore the possibility at your peril.

Oh, but there is FDIC insurance. Take a look at how much money the FDIC has compared to the potential losses. Their cash would be depleted in a heartbeat. Oh, but surely the government would step in. That same government with unfunded liabilities of over $100 trillion? How about the central bank? You mean the insolvent Fed?

Everyone with wealth held in any form, particularly credit (cash, notes, bonds, mortgages, etc.), needs to carefully assess the asset allocation. It won’t take many more events like we have seen this week before the Tsunami of credit destruction shows up. It could be just around the corner.

Consider yourself warned.